You just sold a rental property for $800,000. You bought it for $300,000. That is a $500,000 gain sitting in your hands. Without a plan, the IRS takes a large cut. But there is a legal way to defer that tax. Understanding the 1031 exchange rules can save you tens of thousands of dollars in a single transaction. Many investors lose money simply because they miss a deadline or skip one step. This guide walks you through every rule, timeline, and strategy you need in 2026 to defer capital gains and keep your equity growing.

What Is a 1031 Exchange in Real Estate?

A 1031 exchange gets its name from Section 1031 of the Internal Revenue Code. It lets real estate investors sell one investment property and buy another. The key benefit is that you defer capital gains tax on the sale. You do not eliminate the tax. You push it forward to a later date.

This strategy is also called a 1031 tax deferred exchange. It has helped investors build wealth for decades. The core idea is simple: keep your equity working instead of handing it to the IRS.

Real-World Example: A landlord in Texas sells a duplex for $600,000. He bought it for $200,000. Instead of paying tax on a $400,000 gain, he rolls the proceeds into a new apartment building. He defers the entire tax bill.

Learn more: Explore how GATP Solutions helps real estate investors apply 1031 exchange rules the right way.

How Does a 1031 Exchange Work? Step by Step

Following the 1031 exchange rules means following a clear and strict sequence. Miss one step and your exchange fails. Here is the full process:

- Step 1: Sell your current investment property. This is called the relinquished property.

- Step 2: Hire a Qualified Intermediary before the sale closes.

- Step 3: The Qualified Intermediary holds the sale proceeds. You cannot touch the money.

- Step 4: Within 45 days, identify your replacement property in writing.

- Step 5: Within 180 days, close on the replacement property.

- Step 6: The Qualified Intermediary transfers the funds to complete the purchase.

Every step above is required by the 1031 exchange rules. There are no shortcuts.

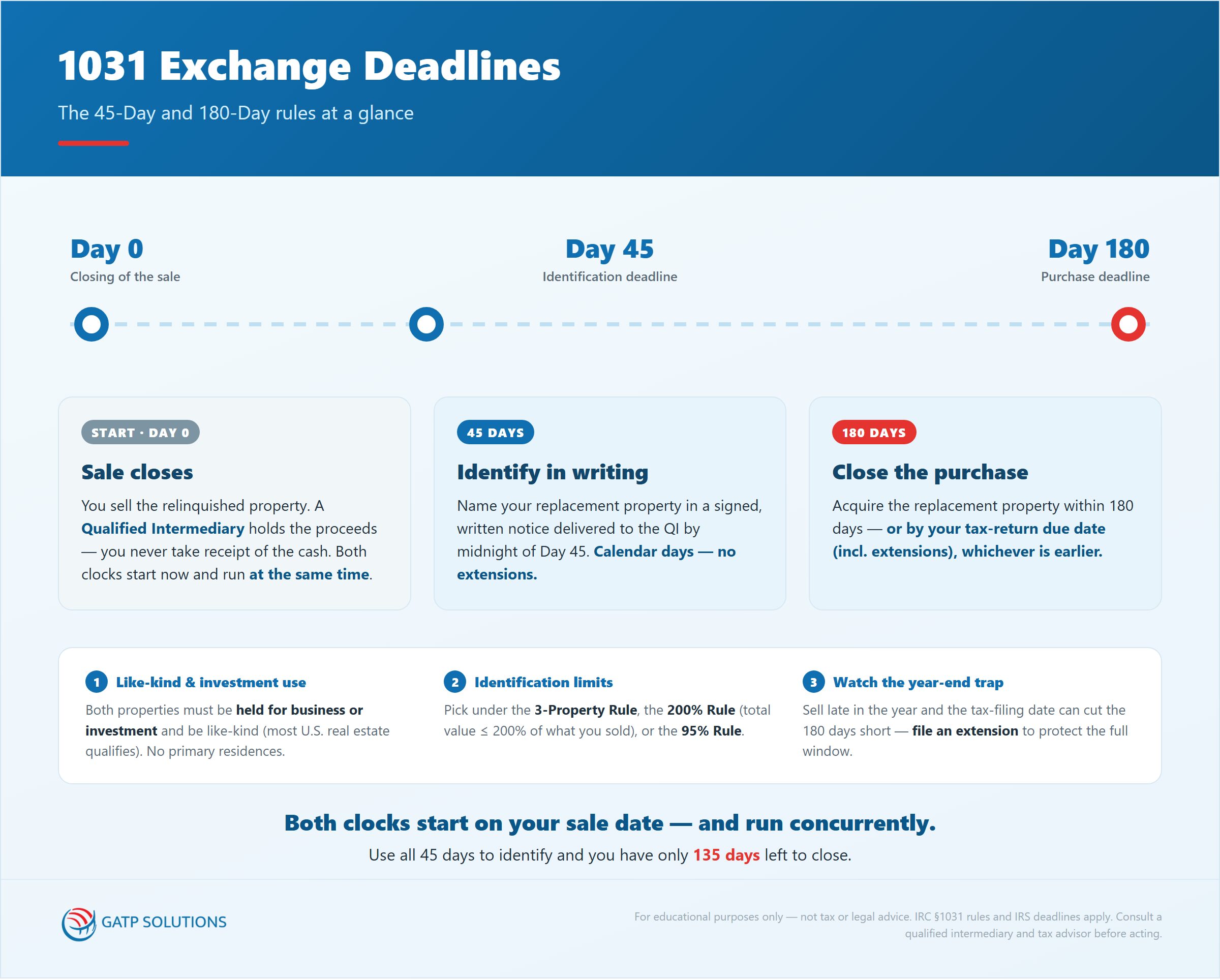

The 45-Day Identification Rule

You have exactly 45 days from your sale date to identify replacement properties. This deadline is firm. The IRS does not grant extensions. You must submit your identification in writing to your Qualified Intermediary. Verbal agreements do not count under the 1031 exchange rules.

The 180-Day Closing Deadline

You have 180 days from the sale date to close on your replacement property. The 45-day and 180-day clocks run at the same time. If you use all 45 days to identify, you have only 135 days left to close.

The Three Identification Rules

The 1031 exchange rules give you three ways to identify replacement properties:

- 3-Property Rule: Identify up to 3 properties of any value. Most investors choose this option.

- 200% Rule: Identify any number of properties, but their total value cannot exceed 200% of your sold property.

- 95% Rule: Identify any number of properties, but you must close on at least 95% of their total identified value.

What Is Like-Kind Property? What Qualifies and What Doesn’t in 1031 Exchange Rules

The 1031 exchange rules require that you exchange like-kind property. The definition is broader than most investors think. Any real property held for investment or business use qualifies. You can swap a single-family rental for a commercial building. You can exchange vacant land for an apartment complex.

What does not qualify under 1031 exchange rules:

- Personal residences

- Vacation homes (unless rented consistently as an investment)

- Inventory or property held for resale

- Stocks, bonds, or partnership interests

Real-World Example: A California investor sells a strip mall for $1.2 million. She uses the proceeds to buy two rental homes in Texas and Arizona. Both homes qualify as like-kind property for a 1031 exchange in real estate. Her gain is fully deferred.

Learn more: See GATP Solutions’ 1031 exchange California compliance resources for state-specific guidance.

The Role of the Qualified Intermediary

One of the most important 1031 exchange rules requirements is using a Qualified Intermediary. You cannot handle the sale proceeds yourself. The Qualified Intermediary is a neutral third party who holds your money between the sale and the purchase. This person cannot be your attorney, accountant, or real estate agent. They must be fully independent.

Choosing the wrong Qualified Intermediary is one of the most common reasons a 1031 exchange investment property transaction fails. If the Qualified Intermediary is disqualified, your entire exchange collapses.

Guarantee Regulatory Compliance Assurance: At GATP Solutions, we ensure all tax filings, payroll, and financial reports meet compliance standards. If an error on our part results in a financial penalty, we cover the cost.

Types of 1031 Exchanges Rules

The 1031 exchange rules apply differently depending on the type of exchange you choose.

Delayed Exchange

This is the most common type. You sell your property first, then buy the replacement. You follow the standard 45-day and 180-day deadlines.

Reverse Exchange

Here, you buy the replacement property first. Then you sell your current property. You need an Exchange Accommodation Titleholder to hold the new property temporarily during the process.

Improvement Exchange

Also called a construction exchange. You use the sale proceeds to build or improve a replacement property. All improvements must be completed within the 180-day window.

Simultaneous Exchange

Both properties close on the same day. This type is rare. It requires very precise coordination between all parties and leaves no room for timing errors.

1031 Exchange Types Compared

| Exchange Type | How It Works | Key Requirement | Timing | Best Fit For |

| Delayed Exchange | You sell first, then buy the replacement. | Standard 45-day and 180-day deadlines. | Sell before you buy. | Most investors. The simplest path. |

| Reverse Exchange | You buy the replacement first, then sell your current property. | An Exchange Accommodation Titleholder holds the new property. | Buy before you sell. | Investors who find the perfect property before selling. |

| Improvement Exchange | You use the proceeds to build on or improve the replacement. | All improvements finish inside the 180-day window. | Build within 180 days. | Investors upgrading or developing a property. |

| Simultaneous Exchange | Both properties close on the same day. | Precise coordination between every party. | Same-day close. | Rare deals with tight, controlled timing. |

Learn more: Read about real estate exchange strategies at GATP Solutions.

What Is Boot and How Do You Avoid It?

Boot refers to any non-like-kind value or cash you receive during the exchange. If you receive boot, you pay tax on that amount. Boot is one of the most misunderstood parts of the 1031 exchange rules.

Common sources of boot:

- Taking cash out of the sale proceeds

- Buying a replacement property worth less than the property you sold

- Taking on less debt on the new property than you had on the old one

Real-World Example: An investor sells a property for $500,000 and buys a replacement for $450,000. The $50,000 difference is taxable boot. He pays capital gains tax on that $50,000 in the year of the exchange.

To avoid boot, your replacement property must be of equal or greater value. Your debt on the new property must also match or exceed your old debt.

Depreciation Recapture and Basis Carryover

When you use a 1031 exchange, your tax basis carries over to the new property. Depreciation recapture does not disappear. It defers until you sell without completing another exchange.

At that point, you owe depreciation recapture tax at 25% on the accumulated amount.

Many investors combine the 1031 exchange rules with cost segregation studies. This strategy accelerates depreciation on the new property and helps offset deferred recapture. It is one of the strongest tax-stacking approaches available to real estate investors today.

Learn more: Explore cost segregation and 1031 exchange strategies at GATP Solutions.

1031 Exchange Rules 2026: OBBBA Tax Law Update

The One Big Beautiful Budget Act introduced several tax changes in 2025. As of 2026, the 1031 exchange rules for real estate remain fully intact. A proposal to cap exchanges at $500,000 per year did not pass. Investors still enjoy full deferral on 1031 investment properties.

However, depreciation recovery schedules did change. Working with a qualified tax advisor ensures you stay current and your exchange documents reflect the latest requirements.

Financial Reports Delivered on Schedule: Monthly, quarterly, and annual reports delivered without delays. If we miss a compliance deadline due to our fault, we pay a 50% fee.

Learn more: Passive Activity Loss Rules for Rental Property.

How to Report a 1031 Exchange: Form 8824

You must report your exchange to the IRS using Form 8824. This form covers the following:

- The property you sold and its details

- The property you acquired and its details

- The complete timeline of your exchange

- Any boot you received during the process

File this form with your annual tax return for the year the exchange was completed. Missing this form can trigger an IRS audit. It is one of the most overlooked 1031 exchange requirements.

Learn more: Contact GATP Solutions to handle your Form 8824 filing accurately and on time.

Common Mistakes That Disqualify a 1031 Exchange

Here is a checklist of mistakes that can invalidate your 1031 exchange rules:

- Missing the 45-day identification deadline

- Touching the sale proceeds before the exchange completes

- Working with a disqualified Qualified Intermediary

- Identifying properties that do not meet the like-kind requirement

- Not filing Form 8824 with your tax return

- Exchanging a primary residence instead of an investment property

- Failing to carry over your adjusted basis to the new property

Real-World Example: A San Diego investor sold her rental property. She forgot to hire a Qualified Intermediary before closing. She took the sale funds directly into her personal bank account. The IRS disqualified her exchange. She owed $180,000 in capital gains tax that same year.

Avoid this outcome by working with an experienced tax compliance team from day one.

Conclusion

The 1031 exchange rules are one of the most powerful tools available to real estate investors in the United States. They allow you to grow your portfolio and defer taxes indefinitely. But the rules are strict. Deadlines are firm. Mistakes are expensive and often irreversible.

Whether you are planning a delayed exchange, a reverse exchange, or exploring 1031 exchange options like Delaware Statutory Trusts, getting the details right is everything. The 1031 exchange rules in 2026 have not changed in your favor, and they do not grant exceptions for honest mistakes.

At GATP Solutions, we ensure full compliance with every exchange we support. Our Guarantee Regulatory Compliance Assurance protects you from costly errors. Our on-time delivery guarantee means your filings never fall behind.

Ready to Defer Your Capital Gains in 2026? Book a Free Consultation and let us show you how to protect your real estate gains.

Frequently Asked Questions – 1031 Exchange Rules 2026

What happens when you sell a 1031 exchange property?

When you sell a 1031 exchange property without completing another exchange, all deferred capital gains and depreciation recapture become due. You pay tax on the full accumulated gain in that tax year. The only way to continue deferring is to roll into another qualifying property.

What is the 1031 exchange timeline?

The 1031 exchange timeline includes two key deadlines. You have 45 days to identify a replacement property and 180 days to close on it. Both clocks start on the exact day you sell your relinquished property.

What is the 2-year of 1031 exchange rules?

The 2-year 1031 exchange rules applies to related-party exchanges. If you exchange property with a family member or related entity, both parties must hold their properties for at least 2 years. Selling before that point triggers the full deferred tax immediately.

What are the 1031 exchange requirements?

The key 1031 exchange requirements include: the property must be held for investment or business use, a Qualified Intermediary must be used to hold funds, both the 45-day and 180-day deadlines must be met, and the replacement property must be of equal or greater value with equal or greater debt.

Why do people do a 1031 exchange?

Investors use a 1031 exchange to defer capital gains tax, preserve equity, and grow their real estate portfolio faster. It also offers strong estate planning benefits through the step-up in basis at death, which can eliminate the deferred tax entirely for heirs.

What is a Delaware Statutory Trust and does it qualify for a 1031 exchange?

A Delaware Statutory Trust is a legal entity that holds real estate and allows multiple investors to co-own property passively. The IRS confirmed in Revenue Ruling 2004-86 that Delaware Statutory Trust interests qualify as like-kind property under the 1031 exchange rules. They are a popular option for investors who want passive income and professional management without active ownership responsibilities.